As the automotive sector adapts to rising vehicle prices, shifting consumer behavior, and persistent inflation, the ripple effects are clearly visible in commercial credit activity. Experian’s latest Commercial Pulse Report (July 22, 2025) dives deep into the evolving credit dynamics within the auto industry—and one trend is clear: credit access is contracting across nearly every segment.

Used Cars Rise, But Credit Lines Fall

With the average new vehicle price exceeding \$47,000, many consumers are opting for used cars, priced more affordably at just over \$28,000. This shift has helped drive consistent growth in the used-car market, accompanied by an uptick in business activity and a growing demand for commercial credit.

In fact, used-vehicle and aftermarket service providers have seen commercial credit inquiries jump approximately 20% above January 2021 levels. Their credit utilization rate now sits at 32%, reflecting the costs of managing larger inventories and higher parts prices. But unlike traditional signs of financial distress, this trend appears tied more to operational needs than liquidity crunches.

Despite the increased appetite for credit, credit limits are shrinking.

A Cross-Sector Credit Contraction

Across the entire automotive supply chain, from OEMs to aftermarket shops, businesses are receiving smaller commercial credit lines on new originations than in previous years. The declines are significant:

- OEMs and New-Vehicle Dealers: Average commercial card limits have dropped by \$7.6K, now sitting at \$9.7K compared to \$17.4K in 2022–2023.

- Used-Vehicle Dealers and Aftermarket Services: Limits have fallen by \$5.8K, from \$13.6K to \$7.8K.

- Vehicle and Parts Wholesalers: These businesses faced the steepest cut—\$8.9K on average, down from \$18.5K to just \$9.6K.

All subsectors experienced over a 40% reduction in average credit lines, signaling tighter lending conditions despite robust business activity in several parts of the industry.

Why Are Credit Lines Shrinking?

This broad contraction is not purely about borrower risk. In fact, many used-car and aftermarket businesses have maintained steady commercial risk scores, and delinquency rates remain relatively flat.

A few critical factors include:

- Elevated Interest Rates: High financing costs are squeezing margins, especially for OEMs and franchised new-car dealers, where delinquencies are rising. Lenders may be proactively managing exposure.

- Segment-Specific Risk Trends: OEMs and dealers are facing mounting late-stage delinquencies—91+ DPD rates have nearly doubled since 2022—and their average risk scores are down ~4 points.

- Economic Uncertainty: Despite stable employment and wage growth, inflation, Fed policy, and geopolitical risk (like tariffs) are prompting more conservative credit practices.

- Portfolio Diversification: Lenders may be redistributing credit availability to less volatile sectors or industries with higher recovery potential.

The Middle Squeeze: Wholesale Distribution

Among the three major segments—OEM/New-Car Dealers, Used-Vehicle & Aftermarket, and Wholesale Distribution—wholesalers are caught in the middle. Their delinquency and risk score trends resemble those of OEMs, but their growing credit utilization and inquiry rates mirror the aftermarket segment. This dual exposure to shrinking new car volumes and rising parts demand puts them in a uniquely vulnerable position.

What It Means for Credit Managers and Lenders

These trends underscore the importance of granular credit monitoring. Treating the auto industry as a single credit risk profile is no longer viable. Subsector segmentation—by vehicle type, service focus, or market exposure—is key to understanding which businesses are truly at risk and which remain stable but under credit strain.

For lenders, this is a time to rebalance risk models and align credit policies with real-time sector insights. For businesses, it’s a moment to double down on credit management and strategic planning.

Stay ahead with Experian

- ✔ Visit our Commercial Insights Hub for in-depth reports and expert analysis.

- ✔ Subscribe to our YouTube channel for regular updates on small business trends.

- ✔ Connect with your Experian account team to explore how data-driven insights can help your business grow.

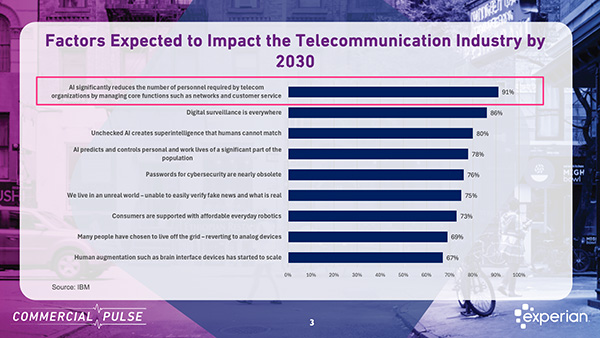

Is AI about to disrupt the telecommunications industry? In this week's Commercial Pulse Report, we explore potential AI disruption in the Telecommunications industry as the transition from analog to digital plays out, and industry consolidation takes hold. Watch The Commercial Pulse Update In 1979, a British new wave band called The Buggles released a song that would become an unlikely cultural landmark. Video Killed The Radio Star wasn’t just catchy—it was prophetic. The lyrics mourned the decline of radio as television and music videos began to dominate how audiences consumed content. Just a few years later, MTV launched, and the shift from audio to visual media was complete. Radio didn’t disappear, but it was permanently changed. One line from the song captures the unease of that moment perfectly “In my mind and in my car, we can’t rewind, we’ve gone too far,pictures came and broke your heart, put the blame on VCR.”The Buggles, 1979 It’s a lament about progress—about technology moving faster than society can comfortably absorb. And it’s a reminder that once disruption takes hold, there’s no rewinding the tape. Fast forward more than four decades, and the irony is hard to miss. MTV itself—once the symbol of disruption—has faded from cultural relevance, ending as it started by playing "Video Killed The Radio Star" on December 31st, 2025. That same cycle defines today’s telecommunications industry disruption, as AI, automation, and consolidation reshape how companies operate and compete. A Familiar Pattern of Disruption Telecommunications has lived through repeated waves of technological upheaval. The shift from analogue to digital fundamentally altered how networks were built, how services were delivered, and how companies competed. That transition drove efficiency, reduced headcount, and accelerated consolidation across the industry. Now, artificial intelligence represents the next inflection point. As highlighted in this week’s Commercial Pulse Report, AI is no longer a future concept for telecom—it’s a near-term operational reality. Industry research shows that a majority of telecom executives expect AI to materially reshape their organizations by automating core functions such as network management, customer service, and fraud detection. Just as video once replaced radio as the dominant format, AI is poised to redefine how telecom companies operate—faster, leaner, and increasingly software-driven. And as history has shown, efficiency gains often come with structural consequences. Consolidation, Scale, and Survival Disruption rarely happens in isolation. It tends to accelerate industry consolidation, and telecom is no exception. Over the past decade, mergers and acquisitions have reshaped the competitive landscape. In wireless, consolidation has resulted in three dominant players controlling the majority of the market. At the same time, the total number of private telecom establishments in the U.S. has declined sharply from its historical peak. This mirrors what happened in media. MTV consolidated attention, then streaming consolidated distribution, and now a handful of platforms dominate content delivery. Each wave reduced the number of viable players while raising the cost of participation. In telecom, AI may lower operating costs—but it also raises the bar for capital investment, data sophistication, and technological capability. Smaller firms face increasing pressure to either specialize, scale, or exit. What the Credit Data Is Telling Us One of the most telling insights from this week’s Commercial Pulse Report comes from telecom credit behavior. Telecom businesses tend to seek credit more frequently than companies in other industries, reflecting ongoing investment needs. However, the average size of credit lines has steadily declined, even as utilization rates have returned to pre-pandemic levels. In other words, telecom firms are doing more with less. This dynamic suggests that businesses may be turning to alternative funding sources, reallocating capital internally, or operating under tighter credit constraints—despite stable demand for connectivity and data services. For risk leaders and growth strategists, this creates a more complex environment. Traditional indicators alone may not fully capture resilience or vulnerability. Understanding industry-specific behavior becomes critical. We Can’t Rewind—But We Can Prepare The line from “Video Killed The Radio Star” still resonates because it captures a universal truth about disruption: We can’t rewind—we’ve gone too far. AI will not undo itself. The telecom industry will not revert to its pre-digital or pre-automation state. Just as radio adapted rather than disappeared, and MTV faded as new platforms rose, telecom companies will continue to evolve—some faster and more successfully than others. The question is not whether disruption will occur, but who is prepared for it. This week’s Commercial Pulse Report explores that question through the lens of macroeconomic conditions, small business credit health, and telecom-specific insights. Together, they offer a clearer picture of how innovation, consolidation, and credit trends are intersecting in early 2026. Because while technology may break hearts along the way, understanding the data helps businesses stay ahead of the next verse. Learn more ✔ Visit our Commercial Insights Hub for in-depth reports and expert analysis. ✔ Subscribe to our YouTube channel for regular updates on small business trends. ✔ Connect with your Experian account team to explore how data-driven insights can help your business grow. Download the Commercial Pulse Report Visit Commercial Insights Hub Related Posts

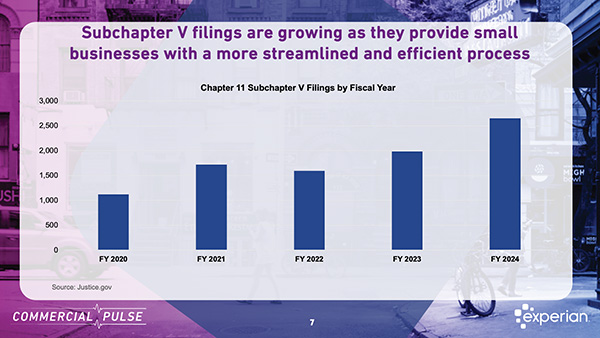

Bankruptcy isn’t just a back-page story anymore, it’s becoming the postscript to the startup surge. The January 27th Experian Commercial Pulse Report reveals a sharp contrast in the small business economy: while business formation remains historically elevated, bankruptcy filings are climbing to levels not seen in a decade. The data points to a critical inflection point—where entrepreneurial growth meets growing financial fragility. Watch The Commercial Pulse Update A Two-Sided Story: Formation and Failure The numbers we see highlighted in the news show a business ecosystem in flux. In December 2025, 497,000 new businesses were launched, a slight dip from November but still 53% above pre-pandemic averages. Since July 2020, an average of 446,000 new businesses have formed each month, underscoring an entrepreneurial surge that has become a defining feature of the post-COVID economy. However, this wave of new businesses comes with significant exposure. Many are lean operations, often led by first-time founders with limited access to capital and minimal financial buffers. These structural vulnerabilities are reflected in rising failure rates. In Q3 2025, business bankruptcy filings hit 24,039—the highest quarterly total since 2016. While some of this activity reflects larger firms restructuring through Chapter 11, a growing share involves smaller, younger businesses taking advantage of Subchapter 5, a newer option tailored for small business reorganization. Understanding Bankruptcy Types: Chapter 7, 9, 11, 12, 13, 15 and Subchapter 5 To better interpret the data, it helps to understand the bankruptcy options available to businesses: Chapter 7 – Liquidation: This is the most straightforward and final form of bankruptcy. Businesses cease operations and a court-appointed trustee sells off assets to repay creditors. Chapter 9 – Municipal Bankruptcy: Exclusively municipalities ( i.e. cities, counties, school districts.) Municipality retains control. No liquidation allowed. No need for disclosure statements. Chapter 11 – Reorganization: This allows a business to continue operating while restructuring its debt under court supervision. Often used by larger or financially complex companies. Chapter 12 – Family Farmer & Fisherman Reorganization: Exclusively for agriculture and fishing operations. Lower cost compared to Chapter 11. Owners keep farm/fishing operation. No need for disclosure statements or creditor committees. Chapter 13 – Individual Reorganization: Primarily for individuals but sometimes used for sole proprietors. Establishes 3 to 5-year repayment plan. Debtor keeps assets and continues operations. Debt limits apply. Chapter 15 – Cross-Border Insolvency: For businesses with assets and creditors in multiple countries. Facilitates cooperation between U.S. courts and foreign courts. Helps protect U.S. assets during international restructuring Subchapter 5 (of Chapter 11): Introduced by the Small Business Reorganization Act of 2019, Subchapter 5 simplifies and lowers the cost of reorganization for small businesses with less than $3 million in debt. Key advantages of Subchapter 5 include: No creditor committee or disclosure statement required Faster court timelines and higher plan confirmation rates Owners can often retain equity Subchapter 5 filings have more than doubled since 2020 and now account for a growing share of all Chapter 11 activity. Who’s Filing—and Why It Matters The report highlights a shift in the types of businesses filing for bankruptcy. These firms are: Small – fewer than five employees Young – under 10 years in operation Low-revenue – earning under $1 million annually These groups now represent the majority of business bankruptcies, showing that financial fragility is highest among the newest and smallest entrants in the market. Early Warning Signs: Commercial Credit Behavior Experian’s commercial credit database reveals clear behavioral patterns among at-risk firms: Higher credit seeking activity: These businesses are 3–4 times more likely to apply for credit before filing. Elevated commercial credit balances: They carry significantly higher balances than non-filing peers. Signs of financial stress: Increased delinquencies and utilization often appear months before a bankruptcy event. This creates an opportunity for lenders to proactively monitor portfolios and identify risk earlier, especially among firms that fit the high-risk profile. What This Means for the Small Business Economy The data paints a complicated picture. New business creation remains strong, driven by structural changes and a resilient entrepreneurial spirit. But these new firms are operating in an increasingly challenging environment, facing inflation, tighter credit conditions, and weakening demand. Subchapter 5 is helping many small businesses stay afloat by making reorganization more accessible. However, rising filings among small and young firms signal that financial strain is becoming more common at the foundational level of the economy. For lenders and risk professionals, the takeaway is clear: track not just the volume of small business activity, but the quality and sustainability behind it. Credit signals remain a powerful early indicator of distress and can help institutions support their small business clients more strategically. Learn More ✔ Visit our Commercial Insights Hub for in-depth reports and expert analysis. ✔ Subscribe to our YouTube channel for regular updates on small business trends. ✔ Connect with your Experian account team to explore how data-driven insights can help your business grow. Download the Commercial Pulse Report Visit Commercial Insights Hub Related Posts

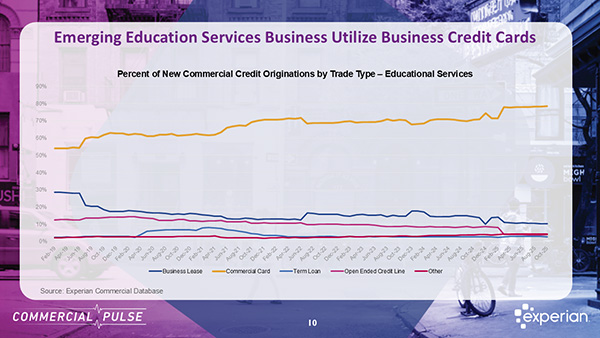

In the just-released Experian Commercial Pulse Report, we focus on a growth small business sector – Education Services, which enjoys healthy, consistent formation, and stable credit management. For Chief Risk Officers navigating an uncertain lending landscape, the question isn't just where growth is happening—it's where growth aligns with manageable risk. The Education Services sector presents exactly that combination, and the numbers tell a compelling story that contradicts conventional wisdom about small business exposure. Watch The Commercial Pulse Update A Sector Transformation Driven by Economic Realities The fundamentals driving Education Services' growth aren't temporary market anomalies; they're structural shifts in how young adults approach career preparation. With youth unemployment rates persistently running more than twice the general population, and young workers facing heightened job security concerns, the demand for skills-based training has fundamentally changed. The traditional four-year degree path is losing its popularity. While bachelor's degree holders still experience lower unemployment rates than those with associate's degrees, the gap has narrowed considerably in recent years. Meanwhile, the escalating cost of traditional college education is accelerating a pivot toward trade schools and specialized training programs, a trend reflected in rising post-secondary enrollment, particularly in trade education. This isn't speculation. Through November 2025, nearly 76,000 new education services businesses have opened— with 7,653 opening in November, the highest level on record. This represents a 205% increase in just two decades. Employment in the sector crossed 4 million for the first time in July 2025. These aren't vanity metrics; they signal sustained, fundamental demand. The Small Business Concentration: Risk or Resilience? Here's where traditional risk models might flash warning signals: businesses with fewer than 10 employees now represent nearly 80% of all educational services firms, up from 63% in 2019. For most sectors, such a high concentration of small businesses would trigger heightened scrutiny and tighter credit controls. But Education Services is defying that conventional risk calculus. Despite this shift in concentration toward smaller operators, credit performance metrics tell a different story—one of discipline and stability that should inform how risk leaders approach this segment. Credit Performance That Challenges Assumptions The credit behavior within Education Services reveals patterns that warrant a fresh risk assessment framework. Commercial credit cards dominate the sector, representing over 78% of monthly originations—a preference that actually provides lenders with valuable visibility into cash flow patterns and working capital management. What's particularly noteworthy: while many industries have experienced tightening credit limits over the past several years, average commercial card limits in Education Services have increased 23% since 2019, now exceeding $19,000. This expansion isn't resulting in overleveraged borrowers. Utilization rates remain relatively low, and average commercial credit scores have held stable throughout this rapid expansion phase. This combination, expanding credit access paired with stable utilization and consistent credit performance, signals something important: disciplined financial management even among newer, smaller operators. For risk leaders, this should prompt a critical question: are your current underwriting models properly calibrated to identify opportunity in this segment, or are they applying broad small business assumptions that miss sector-specific strength signals? Strategic Implications for Risk Leaders The Education Services growth story presents three strategic imperatives for Chief Risk Officers: First, industry-specific risk strategies deliver differentiated insight. Blanket approaches to small business risk assessment will systematically underprice opportunity in sectors like Education Services while potentially overexposing you elsewhere. The stable credit performance despite small business concentration demonstrates that sectoral dynamics matter more than size alone. Second, continuous monitoring beats static underwriting. The rapid composition shift in Education Services—from 63% to 80% small business concentration in just six years illustrates how quickly sector profiles can evolve. Risk strategies built on outdated sector snapshots will either miss growth opportunities or accumulate unrecognized exposure. Real-time portfolio monitoring and dynamic risk modeling aren't optional anymore. Third, growth doesn't automatically mean elevated risk. The Education Services sector challenges the reflexive association between rapid expansion and deteriorating credit quality. In this case, expansion has coincided with improving credit access and stable performance. The key differentiator? Understanding the fundamental demand drivers and recognizing when growth is structural rather than speculative. The Broader Context: Skills-Based Economy Acceleration Education Services isn't growing in isolation. It's responding to, and enabling, a broader economic transformation toward skills-based career pathways. As this transformation accelerates, the sector's role becomes increasingly central to workforce development, suggesting sustained long-term demand rather than cyclical opportunities. For financial institutions, this means Education Services represents more than a near-term growth play. It's a sector aligned with multi-year economic trends, serving businesses that fill a critical gap in how workers prepare for evolving job markets. Moving Forward The Education Services sector demonstrates that growth opportunities and manageable risk profiles can coexist, when you have the right analytical framework to identify them. For Chief Risk Officers, the question is whether your institution's risk infrastructure can recognize these nuances or whether you're leaving opportunity on the table. As 76,000 new businesses enter this sector and credit performance remains stable, the window for strategic positioning won't remain open indefinitely. Competitors with more sophisticated sector-level risk analytics will identify and capture these borrowers first. The data is clear. The opportunity is measurable. The question for risk leaders is simple: what's your strategy for Education Services? ✔ Visit our Commercial Insights Hub for in-depth reports and expert analysis. ✔ Subscribe to our YouTube channel for regular updates on small business trends. ✔ Connect with your Experian account team to explore how data-driven insights can help your business grow. Download the Commercial Pulse Report Visit Commercial Insights Hub Related Posts